U.S. Tariff and Trade Negotiations Update June 19, 2025

The past week has seen significant activity in U.S. tariff and trade negotiations, with developments centered on agreements, ongoing talks, and looming deadlines. Here’s a concise overview of the key events:

- U.S.-UK Trade Agreement Advances: On June 16, President Donald Trump and British Prime Minister Keir Starmer signed an agreement lowering tariffs on U.K. auto and aerospace imports, though steel tariffs remain a sticking point. The deal reduces tariffs on the first 100,000 U.K. auto imports to 10% (from 25%) and eliminates U.S. tariffs on U.K. steel and aluminum, while the U.K. zeros out tariffs on U.S. ethanol. This marks progress toward a broader trade deal, with negotiations ongoing.

- U.S.-EU Talks and Tariff Baseline Concerns: The European Union is increasingly resigned to accepting a 10% baseline U.S. tariff, with negotiators finding it challenging to push for lower rates. The EU’s focus remains on constructive dialogue, but preparations for countermeasures continue, including potential duties on U.S. goods like aircraft and machinery if talks falter. The July 9 deadline for resuming steeper “Liberation Day” tariffs looms, adding urgency to negotiations.

- U.S.-Canada Negotiations Intensify: Tensions with Canada persist, but both sides are leaning toward negotiation. Recent talks between President Trump and Prime Minister Mark Carney have outlined a broad trade platform, focusing on practical solutions rather than overhauling North American trade rules. Canada’s 25% retaliatory tariffs on U.S. goods, including vehicles, remain in place, while the U.S. maintains 50% tariffs on Canadian steel and aluminum. Optimism for a deal was expressed at the G7 summit, with Trump warning of unilateral tariff hikes if progress stalls.

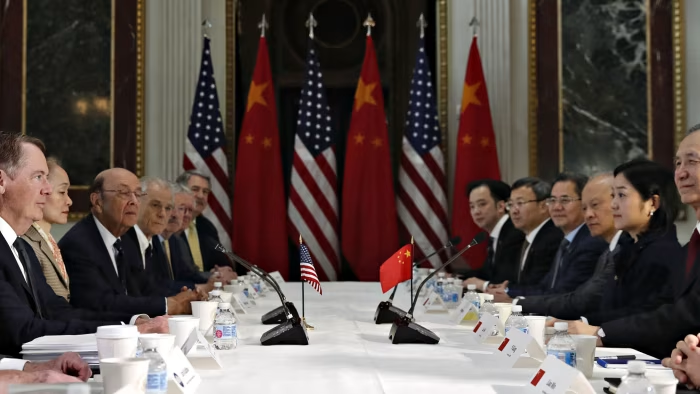

- U.S.-China Trade Truce Holds: Following a May 12 agreement, the U.S. and China maintain a 90-day tariff reduction, with U.S. tariffs on Chinese goods at 30% (down from 145%) and China’s at 10% (down from 125%). This truce, solidified in London last week, includes China easing rare earth export restrictions in exchange for U.S. rollbacks on technology export limits. No new developments were reported this week, but the agreement’s stability remains critical.

- Other Global Talks and Sectoral Tariffs: The U.S. is pushing trading partners for final offers ahead of the July 8 tariff pause expiration. Japan faces pressure, with Trump calling its negotiators “tough,” while over 70% of Japanese firms report minimal tariff impact so far. Sectoral tariffs, including 50% duties on steel and aluminum (expanded to appliances like refrigerators on June 23) and anticipated semiconductor tariffs, continue to shape negotiations.

Economic Context and Outlook: Federal Reserve Chair Jerome Powell noted that tariffs are complicating inflation control, with core PCE estimates for 2025 rising. The U.S. Court of Appeals for the Federal Circuit’s stay on a ruling against Trump’s use of the International Emergency Economic Powers Act keeps tariffs in place pending a July 31 hearing, fueling uncertainty. Global GDP growth forecasts for Q4 2025 are down to 1.4%, reflecting trade disruptions.

With deadlines approaching, the U.S. is balancing aggressive tariff policies with strategic negotiations, aiming to reduce trade deficits while navigating global retaliation risks. Businesses and markets remain on edge as talks progress.